Real Estate Market Update for Queens, NY, for Q3 of 2022

Of course, the salient macroeconomic factor during this quarter was inflation and its continued increase. Core inflation, which is the Consumer´s Price Index minus food and energy, did go up to 6.6% in September, Year over Year. This is despite all the measurements the Federal Reserve is taking to lower inflation, mainly increasing the Fed Fund Rate. This in turn is affecting all other rates, directly or indirectly, like the mortgage rates.

Source, US Bureau of Labor Statistics.

https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category.htm

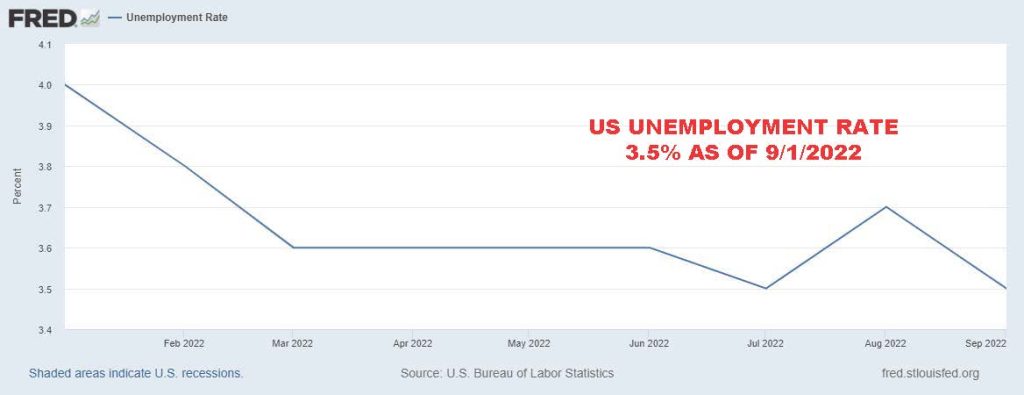

The idea behind increasing these rates is that the cost of money will increase, putting a break to an overheated economy with runaway prices (inflation). The downside is that the adjustments used to tame inflation may weaken the economy too much and start a recession. But the economy has been resilient, and one of the facts that illustrate that, is how resilient job creation has been to the increase in interest rates. Hiring is still happening, and unemployment numbers are at a record low.

Source St. Louis Fed : https://fred.stlouisfed.org/series/UNRAT

Mortgage interest rates, which, as we said, are indirectly affected by the Feds actions, have been increasing tremendously since the beginning of the year. Thirty year mortgage rates have gone up from 3.22% on January 6, to 6.7% on September 29, according to FreddieMac. This means this rate has more than doubled in less than 9 months. The impact on real estate financing and the real estate market was well expected: buyers would have a harder time to qualify for a given mortgage amount and this would put a break on the demand for real estate. Eventually, the frenzy that we experienced in real estate sales would come to a stop, and inventory would start to build up. This is a process, so it does not happen overnight and the indicators for sale prices and transaction numbers are lagging indicators, meaning there is a delay on the way they are reported. In other words, a house that closed today at a price of $800,000 was really negotiated 2 months ago when it went to contract and economic conditions including interest rates, supply and demand, etc., may be different now than they were then. As we will see, the numbers for the Third Quarter of 2022 in the Queens Real Estate Market will show exactly this: a decrease in transaction numbers, an stabilization in price levels and a build up of inventory, signaling the start of a buyer´s market.

Source Freddie Mac: http://www.freddiemac.com/pmms/

However, even though the mortgage rates have a very marked effect in the supply and demand of housing, we need to note that there are other forces at play. One of them is the strength of the dollar relative to other currencies. This makes foreign investors very eager to invest in US real estate, because their local currency is losing value while the dollar is appreciating. Queens is a truly diverse county with investors from all over the world and many foreign buyers have a strong motivation to bring money from overseas to put it in real estate. They are being more cautious and negotiating better terms than 9 months ago, but they are still active in the market.

The Strength of the Dollar makes US Real Estate attractive to foreign investors.

The other force that is supporting values and not letting them accelerate on the way down as fast as one would think given the increase in interest rates is the strong recuperation of the rental market. As we mentioned in previous reports, the pandemic had a detrimental effect on rents, vacancy levels and residential multifamilies. But now with the pandemic in the rearview mirror, rents are higher, apartments are scarce, and everyone is returning to the big cities, including to work and to play. In Queens in particular the median rent in September 2022 was $2,400, up 4-4% from a year ago.

Source: Research done by Manuel Vargas with the One Key Multiple Service data

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

As you know, I like to break down the statistics for residential properties by number of families and property type. The reason for that is that the market changes affect different properties in a unique way. So let´s start with 1 family homes in the third quarter.

Source: Market Report performed by Manuel Vargas., Lic. Broker Associate with data

Provided by the One Key Multiple Listing Service.

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

We can draw the following conclusion by looking at the table above:

- Median Sales Prices for 1 families seem to have stabilized as the quarter progressed.

- In every month of the quarter prices appreciated tremendously year over year.

- But the pace of this appreciation was less pronounced as the quarter progressed.

- Transaction numbers were much lower than at this time of the year in 2021.

So we can say that prices seem to be reaching a peak and while not coming down as of yet ,1 family homes are selling more slowly than at the previous year. The reason for this maybe in the higher mortgage rates and the fact that 1 family homes are purchased by users, meaning homeowners that intend to live in them, and not as much for investment, at least in the Queens market (in other states, 1 families are a popular choice for investors). So 1 family homes do not benefit, as much, from the increase in rental prices in our areas.

Now let´s talk about what happened to 2 family homes.

Source: Market Report performed by Manuel Vargas., Lic. Broker Associate with data

Provided by the One Key Multiple Listing Service.

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

This is a category that is both popular amongst first time home buyers / users (meaning buyers that intend to live in one unit as a personal residence and rent the other unit to help pay for the mortgage) and investor type of buyers (be it cash investors or investors that buy with financing, with the intention of renting both units and holding the property long term). The reason for this is because with rents being so high in NYC and Queens in particular, the rental for the second unit more than compensates the difference in price between a 1 family and a 2 family. To put it another way, 1 families are a little bit of a luxury for the first time home buyer in Queens. Many of my past clients started buying a 2 family in areas close to train and public transportation (Astoria, Jackson Heights, Corona, Elmhurst, Woodside, East Elmhurst, Maspeth, Glendale, Ridgewood, Woodhaven, Richmond Hill, Jamaica, etc.) and then, when they got promoted at work, or got married and became a 2 salary household, they moved up to a 1 family located in more suburban type of areas (Bayside, Whitestone, Fresh Meadows, Little Neck, Douglaston, Cambria Heights, Queens Village, Bellerose, etc.). These are the conclusions about 2 families that we can draw from reviewing the above chart:

- Prices went up slightly or stabilized during the quarter.

- Prices went up around 9% year over year in each of the months, which is remarkable.

- Transaction numbers felt down compared to the numbers for the previous years in each month this quarter and at by double digits in September of 2022 vs. September 2021.

So 2 families were stronger than 1 families presumably because of the comeback and health of the rental market in Queens. However, they were not insulated by the effects of higher mortgage rates and so transactions declined year over year. It is important to note that much of the adjustments that we are seeing in prices and transactions is mostly a return to normalcy. An appreciation of 10% a year is not sustainable in any way, shape or form, and it reflects special economic conditions (low financing rates) and cannot continue indefinitely. As much as we all complained about the lack of inventory for the past 2-3 years, the reality is that we had plenty of inventory, but it was just turning over too fast. The proof is that transaction numbers were at records both in Queens and nationally. The fact that now we have less transactions is to be expected. Like my first broker used to say: “People don´t move every day”. So basically, we sold houses in the last 2-3 years that we were supposed to sell in the future and so now, we have less transactions.

Let´s look at 3 and 4 families. You may ask why do we bunch them together? It is because they have a lot of similarities and because they do not constitute a large group of transactions. If we look at the graph below, we can determine that:

- Median prices did go up towards the end of the quarter.

- Median prices were also higher year over year but they did not experience the boost that two families experienced.

- Transaction numbers were up in July and August, but down in September, year over year.

If I had to explain this, being an experienced landlord I would say that this type of property, let´s call it “small multifamilies”, and which are very popular amongst investors, did get a boost from the rental market bonanza, but not as much as 2 families. They are more expensive to finance because banks usually penalize the fact that you are depending on more rentals to pay the mortgage and because you may be an investor. So when the mortgage rates go up, the “hits” these properties receive because they are perceived as riskier assets for mortgagees have a stronger impacts. In addition to that, some creative financing programs start disappearing when secondary private investors lose appetite for real estate mortgages and most of the mortgages have to backed by Fannie and Freddie. Let´s not forget that we have had tremendous inflation in 2022 which have affected construction materials and energy prices specifically. These may be putting a dent in the landlord business in Queens because of the higher cost of maintenance. And although rents have gone up to record levels, NYC regulations and requirements for landlords seem to continue to increase as well. Again, opposing forces at work.

Source: Market Report performed by Manuel Vargas., Lic. Broker Associate with data

Provided by the One Key Multiple Listing Service.

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

If we look at the increase in transactions in July and August one may say that savvy investors that have been present during some of the past real estate cycles in New York City , may have unloaded properties in expectation of a market adjustment or maybe it was simply because it was a good time to cash out in an asset that had appreciated tremendously and that it ever becomes more burdensome to manage. I am just saying.

Condos and Coops are put together in one category because of their similarities but honestly, more due to the constraints of time an space. I bet that if we would separate them in two different categories we would find different trends and destinies, because Coops are notoriously less “liquid” than Condos. But humor me here and let´s look at the Apartment category:

Source: Market Report performed by Manuel Vargas., Lic. Broker Associate with data

Provided by the One Key Multiple Listing Service.

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

We can note:

- The stabilization of prices. Did they reach a peak? We will know with certainty in the future, but it does looks like it.

- Appreciation year over year stayed slightly above historical standards, but, interesting to note, below inflation levels…

- Transaction numbers declined at the end of the quarter.

We can say that because there is more demand for houses than for apartments in Queens, when prices go up, houses appreciate more for houses and when prices go down, they go down less for houses. It is a fact that I have seen throughout my career. Apartments are usually more difficult to sell and finance because the layers of approval needed by both banking institutions and coop and condo boards.

Our final slide has to do with negotiability and inventory levels:

Source: Market Report performed by Manuel Vargas., Lic. Broker Associate with data

Provided by the One Key Multiple Listing Service.

https://www.onekeymls.com/agent/Manuel-Vargas/679c3f78-0dd8-4a90-9f1b-a4adf8bfc0d8

We can see that:

- Inventory increased towards the end of the quarter.

- The difference between original asking price and final selling price also increased.

- This may reflect the beginning of a buyer´s market.

Again, for those who follow my reports, this comes as no surprise. It is a first a return to normalcy (which is what we are seeing now) and then (to be continued) due to the effect of mortgage rates.

Some of my buyer clients are starting to try to time the market and to ask the question of how much will properties go down given a certain increase in the rate. The answer to this is complicated at best. One of the reasons is that people who bought in the last 12 years, have lower rates than today´s rates and so they are more reluctant to move (sell) if they have to buy another property and pay higher mortgage rate. Yes, you could say some of them got spoilt with record low rates ( 2.6% 30 year fixed!), but the fact is that less inventory will be coming on the market than it would otherwise come if people had been financing with 8-10% rates (like in the early 90´s). So even if we have higher rates now, and we know that they are an adverse factor for home prices, we also have less inventory than in previous years, and this constraint in supply protects home prices up to a point.

What about foreclosures, some of my investors ask? I am not seeing a lot of foreclosures as of yet; to explain that we may look at two factors:

- People who bought in the last 12 years, after the financial crisis of 2009, have bought with different lending standards, meaning real income and downpayments. Like the bankers like to say, they have some skin in the game.

- The appreciation of real estate in the last 12 years has been amazing. According to the appraisal firm Miller Samuel, the median home price in 2010 in Queens was $345,000 (https://ny.curbed.com/2019/12/13/21009872/nyc-home-value-2010s-manhattan-apartments) and in 2019 it was $600,000. According to date from our Multiple Listing, the median price of all residential type of properties (including condos and coops) in September of 2022 was $680,000. That is a tremendous appreciation. So homeowners have equity and therefore, less likely to default on their mortgages.

- The job market is very strong. Businesses are struggling to find workers and unemployment is at record lows. This is another reason why foreclosures may not be as abundant as after the financial debacle of 2008-2009.

Perhaps there may be some foreclosures from buyers who overpaid in their eagerness to compete for a house or the occasional foreclosure due to specific issues of a certain property or personal situations. But I do not see this becoming a general trend, now or in the near future.

Final thoughts.

So, in conclusion, if you live in Queens and pay rent and you are can afford to buy, start gearing up, and I mean by that, getting preapproved and looking at property because you will now have a choice and you will be able to dictate some terms. Given the way rental prices are, there is really no comparison between renting and buying in Queens looking 5 years out. And if you are an investor, thinking of unloading some property that has appreciated well and/or is becoming a hassle to manage, what are you waiting for? And you very well know that as much as you want to get out of the business, the temptation to jump back in will arise when you start seeing opportunities and deals, and those with cash will be better positioned to take advantage.